The UK economy contracted by 0.5% in July, but this reflects one-off factors rather than inherent weakness. Output in the health and education sectors fell sharply due to strikes, which should now be over, while lower output in the distribution and hospitality sectors probably reflects poorer weather dampening demand.

In fact, the latest data revisions show that the UK economy has grown faster than Germany and France in the post-Covid period. Even better, growth in Q2 was led by resilient spending by both consumers and businesses. Some support also came from a rise in government spending, but weakness in trade remains the UK’s Achilles heel.

The outlook is still for sluggish growth this year, followed by a marginal pick up in 2024. Purchasing Managers’ Indices (PMIs) are pointing to a downturn in private sector activity, with the composite PMI at 48.5 in September. That said, the future activity sub-index was at 69.0, compared with 68.9 in August. It seems that businesses are hopeful that an anticipated decline in inflation will support broader economic activity.

Steady improvements in consumer confidence support such a view. The GfK Consumer Confidence Index rose in September, supported by strong wage growth and easing inflation. The recent descent in mortgage rates from their 15-year high also boosted sentiment, while an upturn in an index tracking households’ desire to make major purchases, bodes well for retail ahead of Christmas. In August retail sales increased by 0.4% after falling by 1.2% in July. Meanwhile, the CHAPS card aggregate spend index rose by 0.5% in September.

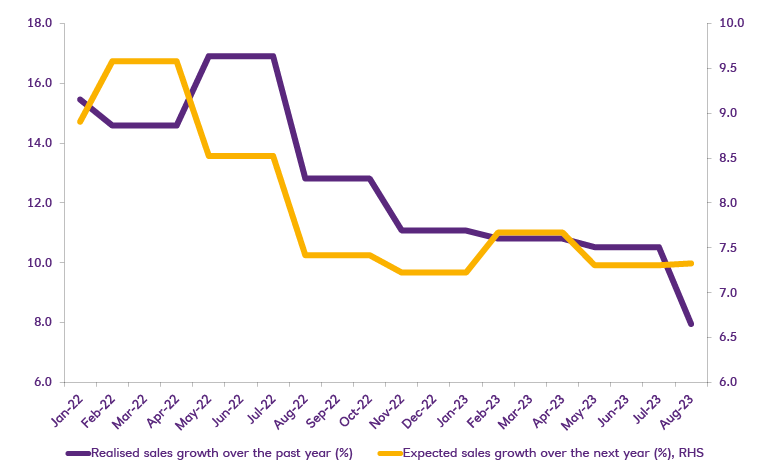

But the economy isn’t out of the woods just yet. Consumer confidence is still well below its long-run average, and the BoE’s Agents Survey shows weak retail volume growth for Q3. Households are trading down to less expensive options, while low housing activity is weighing on demand for household goods. And investment intentions remain weak, owing to pressures on cashflow and margins.

Combining the signals from business and consumer surveys, the outlook remains that of near-term resilience but persistent challenges. The consensus forecast is for growth of just 0.4% this year, followed by another 0.6% in 2024.